Have you heard of the Great Wealth Transfer? The term refers to a significant transfer of wealth that will take place in the coming years. This is resulting from the Baby Boomer generation passing wealth to their children and grandchildren. In Canada alone, the younger generation will inherit about $150 billion before 2026, found RBC Wealth Management. In the United States, that number is closer to a staggering $68 trillion by 2030, says Coldwell Banker. These days, inheritance is big business.

With so many expected to be recipients of this intergenerational wealth transfer, it is essential to understand the specifics behind gifting, leaving and receiving an inheritance, and estate taxes. This guide will answer your questions on how inheritance works in Canada and the tax implications of receiving one.

Table of contents

- Is there a difference between an inheritance and a gift?

- What is the average inheritance in Canada?

- Do you pay inheritance tax in Canada?

- What happens when you receive an inheritance in Canada?

- How long does it take to receive an inheritance?

- What is the best way to invest the money?

- What happens to an unclaimed estate?

- Takeaway

Is there a difference between an inheritance and a gift?

Though they may seem similar, an inheritance and a gift are different. At least they are in the eyes of the law and the tax code.

Inheritances

Inheritance is passed to a beneficiary from the estate after the owner passes away. Assets are distributed according to the will of the deceased. In Canada, inheritance is often received after the will has gone through probate. This certifies that the will is valid, and the executor can proceed to pay out the estate. When applicable, the estate pays any fees associated with the application of probate.

In Canada, anyone over the age of 18 is eligible to receive an inheritance. If the beneficiary is still a minor, assets are held in trust until they reach the legal age.

Download Your Free Guide

6 Tax Strategies for Canadian Investors with $500k Portfolios

Gifts

A gift, on the other hand, is typically transferred from one person to another “intervivos” — meaning while the grantor is still alive. This type of intergenerational wealth transfer is sometimes called a ‘living inheritance.’ There is no gift tax in Canada, so living inheritances are not taxed. It is possible that the grantor will pay capital gains tax on the disposition of the assets, though.

Providing a gift during your lifetime means that you can witness the positive impact that the money or property has on the life of your loved ones. A word of caution, however: once the recipient accepts the assets, you have no further legal claim. There is a deemed disposition and no way to take back the gift for any reason, including if you run out of funds to support your lifestyle.

Receiving an inheritance may feel the same as receiving a gift for the beneficiary, but they involve a different legal process.

What is the average inheritance in Canada?

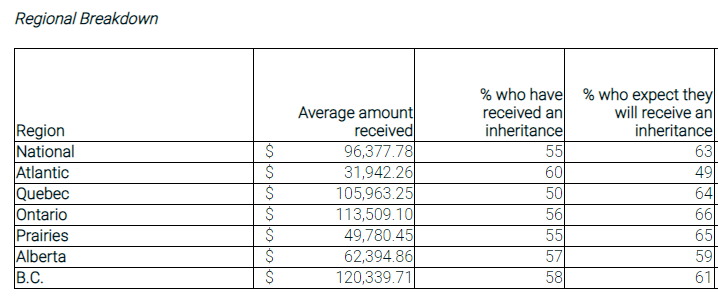

Unfortunately, the information available for how much Canadians expect to receive from an inheritance isn’t very recent. A 2014 survey by BMO InvestorLine found that Canadians expected an average inheritance of just over $96,000. Averages did, however, differ greatly across the country. British Columbians had the highest estimated inheritance with amounts closer to $120,000 on average. Those living in Atlantic Canada anticipated the lowest amounts, closer to $32,000.

Overall, 55% of Canadians surveyed by BMO had already received money as an inheritance, while 63% believed it was imminent. A 2019 Edward Jones found that of the 1,565 Canadians polled, 44% believe they would receive an inheritance in the future.

One thing is clear: while exact numbers differ, a considerable number of Canadians will inherit money in the coming years.

START WORKING WITH A WEALTH MANAGER NOW

Do you pay inheritance tax in Canada?

In short, no. Canada doesn’t have an inheritance tax (sometimes called a “death tax”). This does not mean that there are no taxes due, though. The Canada Revenue Agency (CRA) will instead tax the estate instead of the beneficiary.

The executor must submit a final tax return for the deceased. The estate pays taxes on both income and capital gains earned. Taxes are calculated as if the deceased’s assets were sold on their date of death – also known as ‘deemed disposition.’ In some cases, this might trigger sizable capital gains. From there, assets are distributed among the estate beneficiaries, with no taxes due by the recipients.

For reference, Americans do not pay inheritance taxes on a federal level either. Six states, however, have implemented a tax at the state level.

What happens when you receive an inheritance in Canada?

What will happen when you receive an inheritance in Canada is highly dependent on the way that you receive it. Liquid assets, including bank and investment accounts, are different from illiquid assets, such as real estate or land.

What happens when you inherit money in Canada?

The exact steps depend on the type of account where the assets are initially held. Except for registered investment accounts, the beneficiary only receives money after probate has been granted.

For registered investment accounts — including TFSAs, RRSPs, RRIFs, LRSPs, LIRAs, and LIFs — the owner can designate a beneficiary who will receive the account’s proceeds. A qualified beneficiary can roll the deceased’s account into their own registered account while maintaining the tax-deferred status. In Canada, a qualified beneficiary is a spouse, common-law spouse, or a financially dependent child or grandchild.

When the account owner designates anyone not considered a qualified beneficiary, CRA will tax the owner at the time of their death as if they had withdrawn the entire account at once. The beneficiary named receives the account balance directly, with no further taxes owed at that point. Financial institutions can often undergo this process without a probated will. As a result, you may receive the proceeds quite quickly.

The deceased’s will directs the proceeds of bank accounts and non-registered investment accounts, complicating the process. When applicable, the estate will pay taxes, including capital gains tax, on the account as CRA will consider that there is a deemed disposition of the holdings on the date of death. The executor then directs the account’s proceeds to the beneficiary as identified in the will. In this case, receiving your inheritance could take some time. First, the will must go through probate.

What happens when you inherit real estate in Canada?

There is no inheritance tax on real estate or land in Canada either. The deceased’s final tax return would show a deemed disposition, and the estate will be taxed as if the property was sold at their death.

Once you receive the property, there are no further tax implications until it is sold. You will not owe taxes on the sale if the property is your primary residence for tax purposes, thanks to Canada’s principal residence exemption. If, however, the property is not designated as your primary residence, you are required to pay capital gains tax based on the sale price. Capital gains are calculated as the selling price less the adjusted cost base, or in this case, the property’s fair market value at inheritance.

How long does it take to receive an inheritance?

You may be anxious to get inheritance money left to you and move on. Unfortunately, the process can take time. The executor gathers all necessary documents and files for probate with the courts. Once filed, probate will take at least 3 to 6 months. This does depend on the deceased’s province of residence and the size of their estate. During this process, it is possible to contest the will, though it can add a considerable amount of time. You may be waiting years before you can receive your inheritance.

One important note is that estates that are smaller in size can sometimes apply for expedited probate and, in some cases, may be able to skip probate altogether. If possible, this is advisable as it can save both time and money. For example, in Ontario, a small estate is worth $150,000 or less, and there is a simplified probate process.

In addition to applying for probate, the executor may need to first sell the assets then distribute the funds. Be sure to factor in the time that this will take in your inheritance expectations. For example, selling a house can take much longer than liquidating an investment account held in stocks.

What is the best way to invest the money?

When you are the beneficiary of an inheritance, it can be tempting to take the money and spend it right away. It is often best to wait before making any large purchases or decisions with inherited funds, though. If you are on the receiving end of an inheritance, it also means that you have most likely lost someone close to you. It is more important to grieve than it is to make investment decisions in those first few months.

Download Your Free Guide

6 Tax Strategies for Canadian Investors with $500k Portfolios

How to protect your inheritance

We recommend speaking to your wealth manager when you’re ready. A trusted wealth manager can help to update your financial plan, so it is reflective of your new net worth. From there, you can invest the funds in the holdings that are best for your personal situation. Ultimately, it is a personal choice. One of the best ways to protect your inheritance is by putting the money to work, keeping your risk tolerance and investment objectives in mind.

Related Reading: Tips To Find A Wealth Manager

What happens to an unclaimed estate?

If someone dies without a will, they have died intestate. While they may not have a valid will, it does not necessarily mean the inheritance will go unclaimed. Spouses, children, relatives, and other next of kin can claim the estate. Each province has different intestacy laws that regulate the application process and eligibility of beneficiaries. If there are no eligible next of kin based on the provincial law, the proceeds will become the government’s property — otherwise known as escheat.

It is also possible for a beneficiary to waive their right to inherit or disclaim an inheritance. Should this happen, the executor will distribute the estate amongst the remaining beneficiaries listed in the will. If no other heirs are named, the estate is split according to applicable provincial intestacy law. In the end, the unclaimed inheritance could end up in the government’s hands. This certainly underscores the importance of estate planning and having an up-to-date will.

Takeaway

Gen X, Millennials, and even Gen Z are all about to receive a tremendous amount of wealth. Understanding how inheritance works is critical for both those planning to leave a legacy and those who will be receiving one.

While there is no inheritance tax in Canada, the deceased’s estate must pay taxes as a deemed disposition. Applying for probate, submitting the final tax return, and settling the estate can take some time. As a beneficiary, it is best to be patient. This is especially wise given the emotional nature of the process. In the meantime, rest assured that the inheritance left by your loved one will not be taxed further once it is in your hands.

Suggested Reading: